For years now, insurers have coasted with little to no impact from new and emerging technologies. However, the clock has run down—now’s the time to innovate. Customers finally understand the benefits of new technologies; many change agents are mature enough for implementation at scale, which drives efficiency and improves customer experience. While incumbent insurers have coasted without innovation, disruptors have developed innovative models. Some challenge incumbents, while others look to supplement.

For legacy insurers to remain relevant in the increasingly digital world, they must understand the new breed of competition and adapt their models by working alongside disruptors and pushing their own research and development.

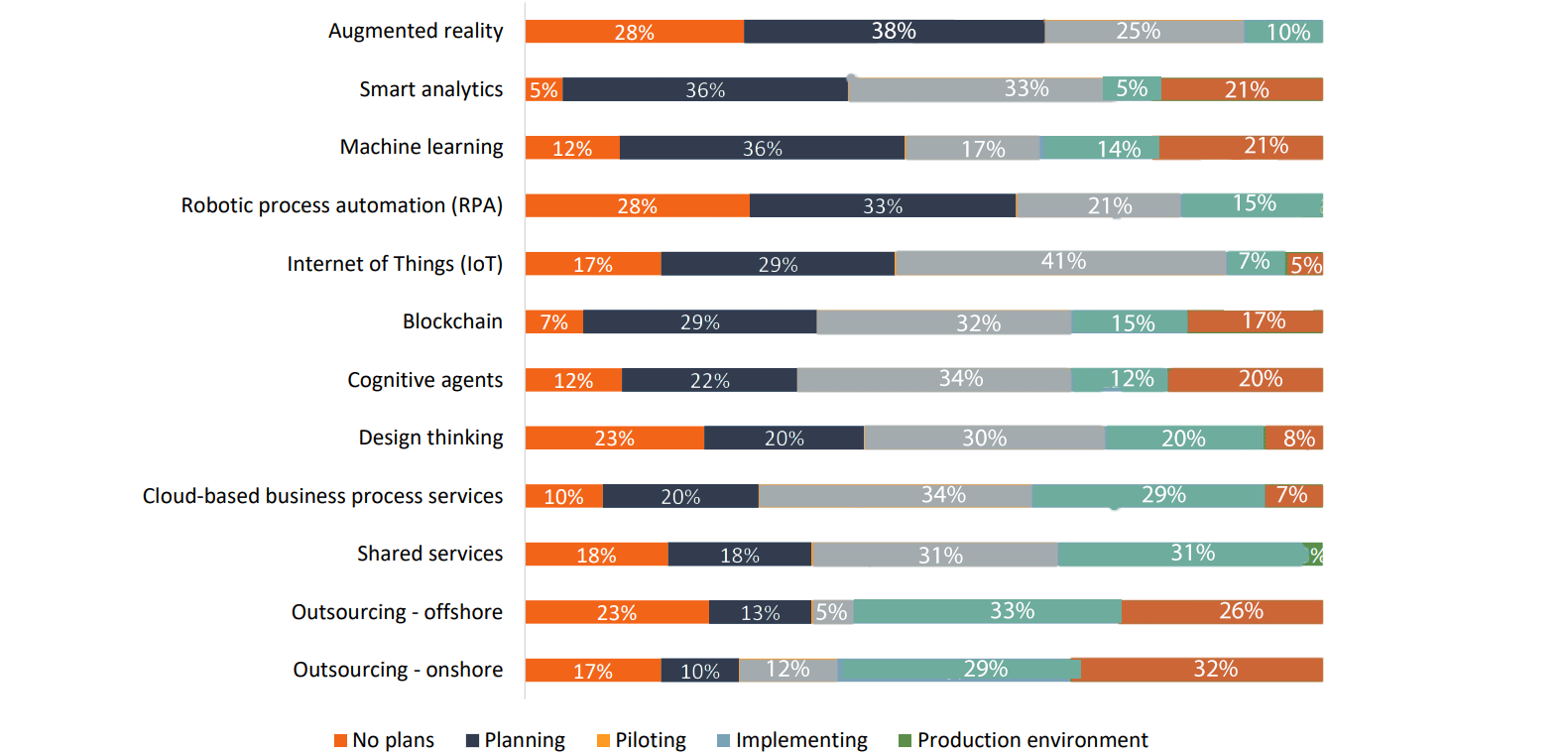

The modern insurance market leaves little room for incumbents to remain stuck in their ways

As customer needs evolve and new technologies break the market’s barriers to entry, insurance becomes an increasingly populated space. A crowded market ramps up pressure on margins; to remain profitable, disruptors and incumbents alike must look for new methods of differentiation.

In reality, the majority of insurers know they can’t remain dormant. Research from Accenture found that 86% of insurers believe their innovation must accelerate to retain a competitive edge. However, despite understanding the desperate need for hasty change, the majority of insurers remain stuck in the planning and piloting phases with leading change agents (see Exhibit 1). In addition, insurtech investment exceeded $3 billion in 2018. It’s clear that insurers simply aren’t prepared for the disruptive onslaught that awaits them.

Exhibit 1: Insurers remain in the planning and piloting phases with leading change agents

Source: HFS Digital Transformation by Industry 2018; insurance n=39

By Miles: Moving beyond the traditional motor insurance model to offer customers the option to pay by the mile, driving down premiums

Automotive insurers currently use an inefficient pricing model that leaves customers paying excessive premiums. Previous HFS research discusses the demand for a “live-time” insurance product. By Miles, a UK-based automotive insurance disruptor, offers a simpler product: pay-per-mile insurance, targeting the UK’s 19 million low-mileage drivers. Its policy has customers paying a fixed yearly fee up front that insures the car when it isn’t in use; beyond this, it insures the vehicle on a pay-as-you-go basis.

The company measures mileage through a telematics device that it sends to the customer when their policy begins. By Miles can then track a customer’s daily mileage and charge accordingly. It caps the total charge at 150 miles per day and 10,000 miles per year, so it does not unfairly charge customers who occasionally travel longer distances.

HFS’ Take – While insurers must understand that customer demands are changing, they all have different needs and demands.

Paying for insurance by the mile will appeal to many, and the success of By Mile is a testament to that. Jaguar Land Rover, AXA, and others have provided support, and the company recently closed a £5 million Series A funding round. However, the UK’s muted response to telematics motor insurance policies tells us that many customers see these policies as an invasion of privacy, in fact RAC Business found that 40% of businesses faced privacy concerns from staff when looking to install similar devices. Furthermore, when a model calculates premiums using a single factor, like mileage, it ignores large amounts of data. A mile a customer drives at 2:00 p.m. in full sunshine is much less risky than a mile he drives at 3:00 a.m. in the snow. So, while the insurance product offers benefits to drivers with low annual mileage, it only goes halfway to offering a truly adaptable insurance policy.

For incumbent insurers, By Mile’s pay-by-mile model must help them understand that customer demands have shifted beyond existing models. If they don’t adapt, their customers will look elsewhere.

Instanda: Innovating insurance system architecture allows insurers to reach new heights of agility

Insurance is complex. Collaboration between many organizations can create longwinded processes; insurers must explore any opportunities to streamline these processes. Founded in 2012, Instanda developed cloud software allowing insurers to create, manage, and distribute insurance products with ease. It claims insurers can create new products on its platform in a matter of days and move existing ones on board within weeks. Exhibit 2 shows Instanda’s key features. It’s clear that the company’s goal is to enable insurers to securely scale their business through streamlining internal processes and prioritizing the customer experience.

Exhibit 2: Instanda’s key features

Source: Instanda website homepage

In fact, while paper-intensive internal processes shackle incumbent insurers and place considerable strains on resources, competitors using Instanda may find the flexibility to focus on their customers and become truly responsive to their needs.

HFS’ Take – OneOffice should be the ambition for insurers but they must remain realistic with their expectations.

Instanda advocates HFS’ Digital OneOffice (see Exhibit 3), which explains how enterprises must break down traditional silos across their front, middle, and back offices to maximize their customer focus. Focusing on customers is a step in the right direction for the insurance industry, as customer centricity has been the missing ingredient for too long.

Exhibit 3: The Digital OneOffice Framework

Source: HFS Research, 2018

However, insurers must question must exactly how easy it is to make the jump to software like Instada; its claims that customers can create new products in days may be true, but it’s likely more difficult to transform existing products, which is potentially disruptive to customers. The emergence of disruptors looking to augment legacy insurers means that the window to select innovative partners is closing. Insurers must act quickly or be left behind by more proactive competitors.

The Bottom Line: If insurers hope to remain relevant in the increasingly digital world, they must recognize key differences in disruptors and co-operate with them.

The insurance industry has remained unphased for too long, and innovative disruptors are shaking up the market. What insurers must learn from the two firms detailed in this piece is that disruption comes in different shapes and sizes. Some will directly challenge their model, while some will supplement it.

Clearly, the time for change is now. Incumbent insurers must recognize that customers’ demands are shifting and vigilantly identify disruptors that can augment their existing models. Furthermore, they must understand that in a homogeneous market, time-to-market and innovation are key—partnering or acquiring disruptors that challenge their model may be their only hope of remaining relevant.